In my Twitter/X account — which basically has five followers — the platform recommended an investment strategy expert, who had an interesting quote: “If you want something new, you have to stop doing something old.” That’s actually an insightful commentary, especially when it comes to modeling the financial markets.

Recently, I have been questioning the viability of the traditional approaches of fundamental and technical analysis. While plenty of debate rages on the topic — especially when it comes to the chart-reading stuff — the undeniable flaw in both systems is that they violate Ashby's Law of Requisite Variety.

A quick Google search will reveal that the cybernetic principle states that “for a system to be effectively controlled, the variety of the controller must be equal to or greater than the variety of the system being controlled.” In other words, a model must be adequately as complex as the environment it purports to explain.

It’s not a law like gravity but it’s unlikely to be false because it’s true by construction. When you consider the equities market, it is stochastic, chaotic, non-linear, heteroskedastic, reflexive and non-ergodic, among many other characteristics. A genuine model must attempt to adequately address probably at least 50% of the market’s categorizations.

Let’s be brutally honest with each other. To say that an industry dominated by liberal arts majors has found the answer to one of the most complex systems in all of human history is stretching incredulity.

Further, when it comes to fundamental analysis, I believe that investors should be skeptical of the two key premises: that the author can reliably predict future cash flows and that the target share price carries a linear relationship with said future flow —and thus collapsing volatility, heteroskedasticity, path dependence, non-stationarity, reflexivity, non-ergodicity and microstructure effects.

I’m not going to sit here and claim that I have the ultimate answer because I don’t. What I will attempt, using a Kolmogorov-Markov framework layered with kernel density estimations (KM-KDE), is forward a non-parametric probabilistic model.

Essentially, we’re going to let the data speak for itself — and consider placing wagers empirically, not emotionally.

MP Materials (MP)

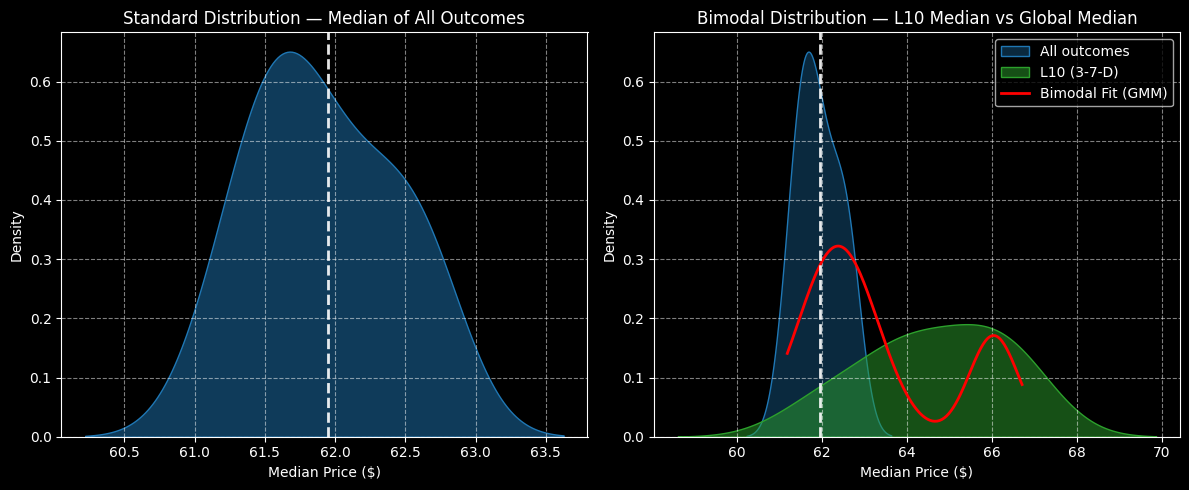

To be upfront, I’ve been talking relentlessly about MP Materials (MP), for both Barchart and other financial publications. Ordinarily, I should just stop beating a dead horse — except that this horse very much has a lot of life left. Using my sequencing logic, MP stock is currently structured in a 3-7-D formation; that is, in the past 10 weeks, MP has printed three up weeks, seven down weeks, with an overall downward slope.

Who gives a hoot, you might say? Here’s where my KM-KDE approach differs in mentality from technical analysis. Right now, MP stock is sandwiched between the 50-day moving average up top and the 200 DMA at bottom. But with no prominent chart patterns, there’s really nothing here for a technician to chew on — unless he or she would like to make something up.

However, under the quantitative approach (KM-KDE), the statistical response to the 3-7-D is different from other sequences (like 7-3-U for instance). One of the biggest differences comes in probability density. Using a reified, iterated logic, price clustering under aggregate (baseline) conditions would likely occur at around $61.70 over the next 10 weeks.

Still, under the principle of heteroskedasticity, different stimuli yield different results. Under 3-7-D conditions, price clustering is likely (though not guaranteed) to occur at $65.50 over the next 10 weeks. Now that we know what’s likely, we use data from Barchart Premier to identify the 60/65 bull call spread expiring Jan. 16, 2026 as a potentially viable target.

elf Beauty (ELF)

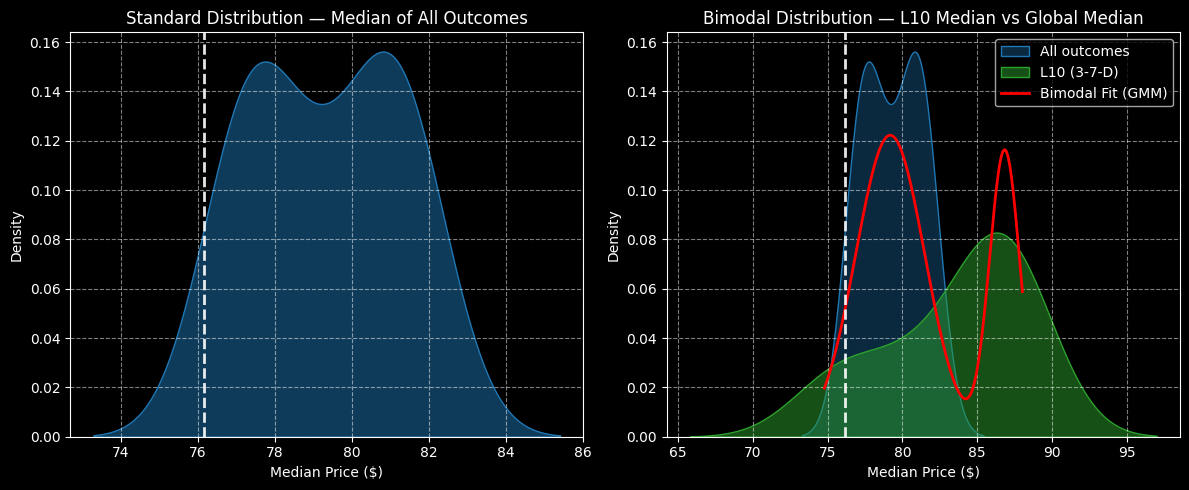

For those who don’t mind taking greater risks, cosmetics giant elf Beauty (ELF) could be a fascinating idea. Yes, ELF stock is wildly risky, especially because it lost more than 39% on a year-to-date basis. Plus, its recent performances have been horrific, with the security losing 40% in the past month. At the same time, speculators are attempting to extract value out of this play. In the past week, ELF is up nearly 12%.

However, what’s really intriguing here is that ELF stock has printed a 3-7-D sequence. Again, under the principle of heteroskedasticity, we know that different stimuli yield different results. Typically, when aggregating 10-week iterated price data going back to January 2019, two clusters occur: one at around $77.90 and the other at $80.90.

But the arbitrage opportunity that we’re seeking is the expected outcome under 3-7-D conditions, not just in the aggregate. When running 3-7-D iterations, prices tend to cluster at $86.50 over the next 10 weeks. So, with that being the case, I’m really loving the 80/85 bull call spread expiring Jan. 16, 2026.

While this spread isn’t a literal arbitrage opportunity, it’s an informational variant. Essentially, the market doesn’t expect the $85 strike to be possible — and thus they’re going to give you a maximum payout of almost 178%.

Bitdeer Technologies (BTDR)

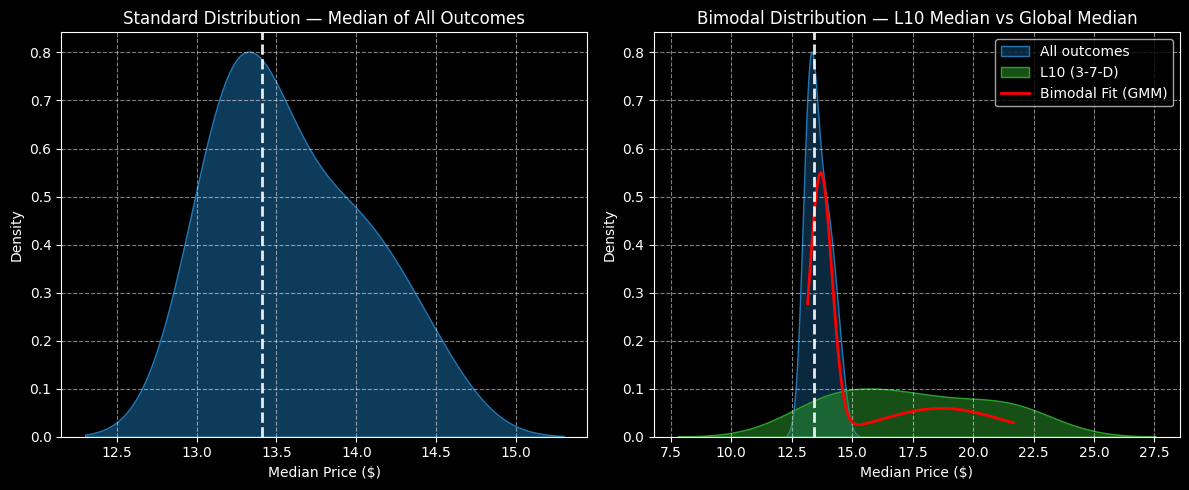

If you’re looking for an admittedly low-confidence, super-high-potential wager, you may want to take a look at Bitdeer Technologies (BTDR). Open Barchart’s profile page on BTDR stock and you’re greeted with the fact that, as of this writing, the security carries a 24% Weak Sell rating. I suspect that this assessment has a little something to do with BTDR losing more than 38% on a YTD basis.

Oh yeah, it’s also down 42% in the trialing month. Being a cryptocurrency and blockchain mining platform, extreme undulations are integrated into the narrative. Being a clear non-ergodic entity, you need to exercise extreme caution with this bad boy.

So, why do I like this volatile mess? As with the other securities on this list, BTDR stock has printed a 3-7-D sequence in the trailing 10 weeks. Under aggregate circumstances, the probabilistic distribution of outcomes over the next 10 weeks is statistically narrow, running between $12.25 and $15.40. Further, price clustering would likely occur at around $13.30, indicating a neutral to slightly bearish bias.

However, under 3-7-D conditions, the principles of heteroskedasticity reveal that the distributional outcomes expand quite dramatically, between $7.50 and $27.50. Yes, there’s a lot of risk involved but the reward potential is exponentially more robust. Further, price clustering occurs on average around $16. What’s interesting, though, is that there’s not much density difference at $16 versus $17.50.

Subsequently, I’m a fan of the 15.00/17.50 bull call spread expiring Jan. 16, 2026. Triggering the higher strike would lead to a max payout of over 257%.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart