The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how government & technical consulting stocks fared in Q4, starting with NV5 Global (NASDAQ:NVEE).

The sector has historically benefitted from steady government spending on defense, infrastructure, and regulatory compliance, providing firms long-term contract stability. However, the Trump administration is showing more willingness than previous administrations to upend government spending and bloat. Whether or not defense budgets get cut, the rising demand for cybersecurity, AI-driven defense solutions, and sustainability consulting should benefit the sector for years, as agencies and enterprises seek expertise in navigating complex technology and regulations. Additionally, industrial automation and digital engineering are driving efficiency gains in infrastructure and technical consulting projects, which could help profit margins.

The 7 government & technical consulting stocks we track reported a very strong Q4. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was 7.7% above.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 8.9% since the latest earnings results.

NV5 Global (NASDAQ:NVEE)

Operating from over 100 locations across the U.S. and internationally, NV5 Global (NASDAQ:NVEE) provides engineering, environmental, geospatial, and technical consulting services to public and private sector clients for infrastructure and building projects.

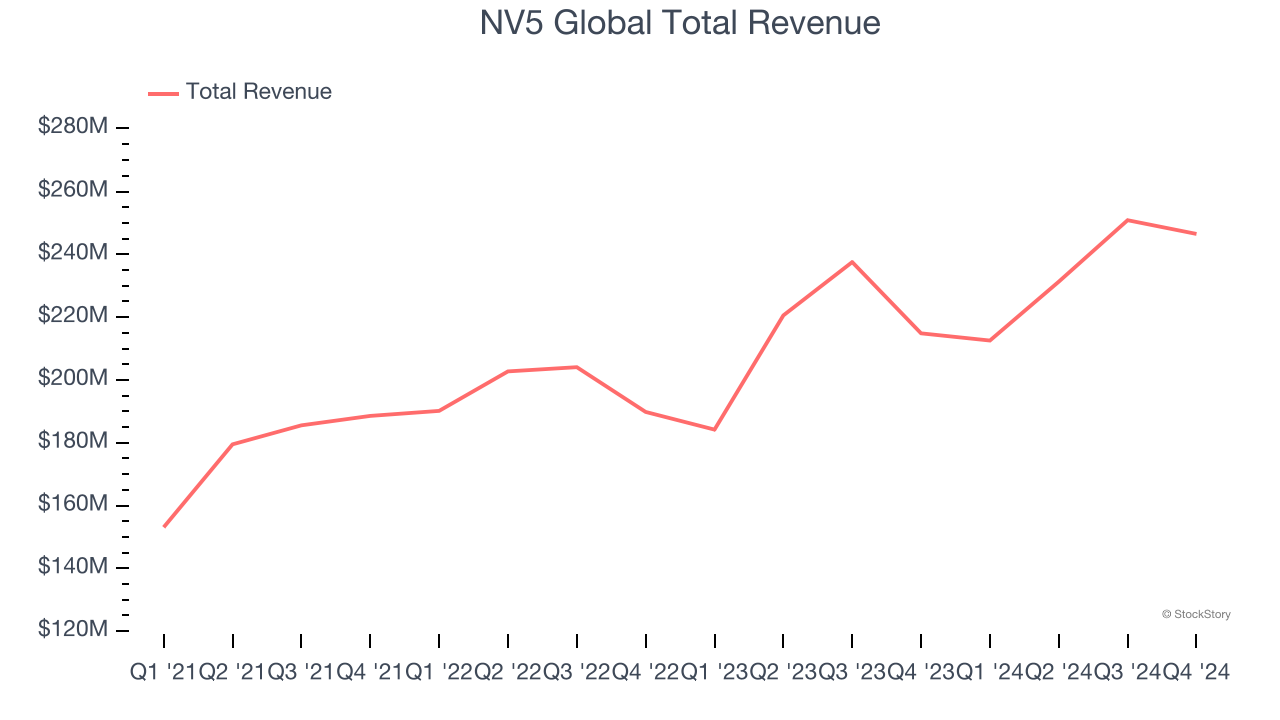

NV5 Global reported revenues of $246.5 million, up 14.7% year on year. This print exceeded analysts’ expectations by 1.6%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ full-year EPS guidance estimates and full-year revenue guidance exceeding analysts’ expectations.

"NV5 delivered a strong performance in 2024, with 10% growth in gross revenues and a 13% increase in gross profit over 2023, and strong organic growth and increased profitability in all three segments of NV5’s business. We enter 2025 with a robust backlog and tailwinds in our target sectors. NV5’s focus on mandated, non-discretionary testing, inspection, and certification (TIC) and engineering services mitigates impacts from economic cycles, and the results of our strategic organic growth initiatives in 2024 continue to drive our growth as we enter 2025. We completed acquisitions in 2024 to strengthen key recurring TIC service areas, including data center commissioning, fire protection consulting, building digitization, and water resources. Our pipeline of acquisition targets remains strong in 2025, and we anticipate further acquisitions to strengthen our platform," said Ben Heraud, CEO of NV5.

NV5 Global achieved the fastest revenue growth and highest full-year guidance raise of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 5.4% since reporting and currently trades at $16.48.

Is now the time to buy NV5 Global? Access our full analysis of the earnings results here, it’s free.

Best Q4: UL Solutions (NYSE:ULS)

Founded in 1894 as a response to the growing dangers of electricity in American homes and businesses, UL Solutions (NYSE:ULS) provides testing, inspection, and certification services that help companies ensure their products meet safety, security, and sustainability standards.

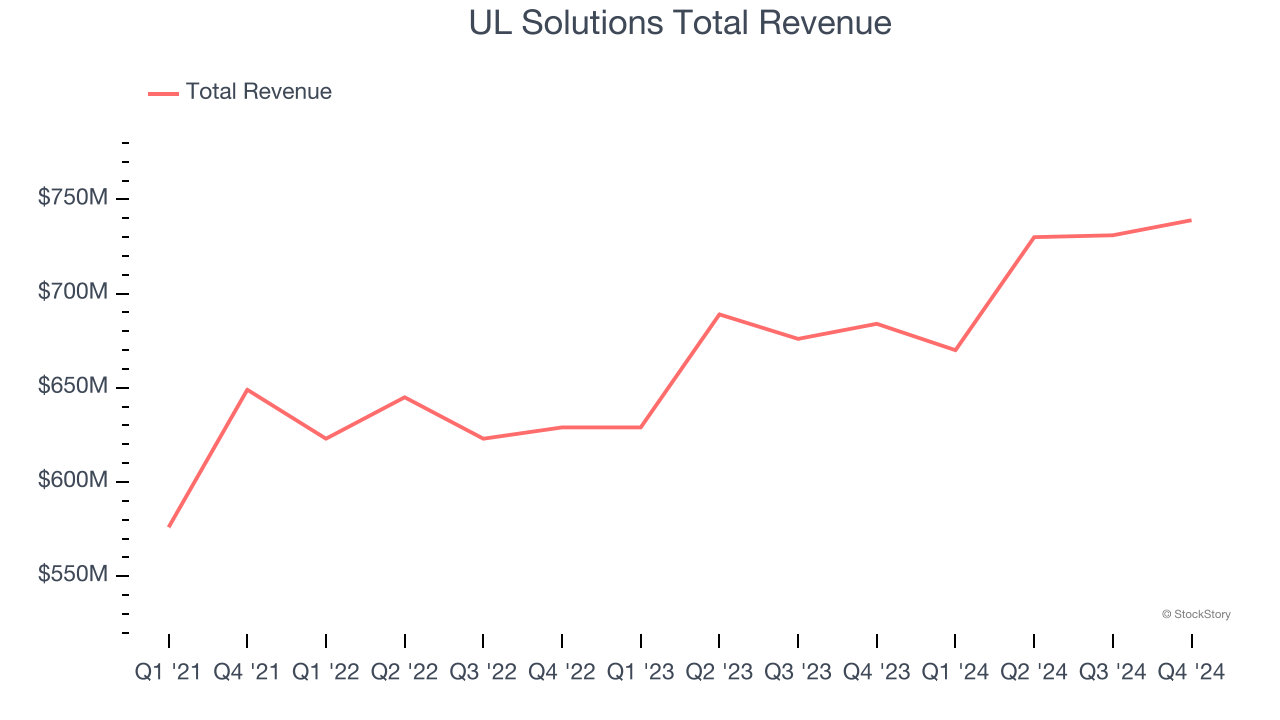

UL Solutions reported revenues of $739 million, up 8% year on year, outperforming analysts’ expectations by 1.9%. The business had an exceptional quarter with an impressive beat of analysts’ EPS estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 2.1% since reporting. It currently trades at $54.35.

Is now the time to buy UL Solutions? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Booz Allen Hamilton (NYSE:BAH)

With roots dating back to 1914 and deep ties to nearly all U.S. cabinet-level departments, Booz Allen Hamilton (NYSE:BAH) provides management consulting, technology services, and cybersecurity solutions primarily to U.S. government agencies and military branches.

Booz Allen Hamilton reported revenues of $2.92 billion, up 13.5% year on year, exceeding analysts’ expectations by 1.7%. It may have had the worst quarter among its peers, but its results were still good as it also locked in an impressive beat of analysts’ organic revenue estimates and a decent beat of analysts’ EPS estimates.

As expected, the stock is down 18.4% since the results and currently trades at $105.26.

Read our full analysis of Booz Allen Hamilton’s results here.

SAIC (NASDAQ:SAIC)

With over five decades of experience supporting national security missions, Science Applications International Corporation (NASDAQ:SAIC) provides technical, engineering, and enterprise IT services primarily to U.S. government agencies and military branches.

SAIC reported revenues of $1.84 billion, up 5.8% year on year. This number surpassed analysts’ expectations by 1.4%. It was a very strong quarter as it also recorded a solid beat of analysts’ EPS estimates and a narrow beat of analysts’ full-year EPS guidance estimates.

The stock is up 7.7% since reporting and currently trades at $112.51.

Read our full, actionable report on SAIC here, it’s free.

Amentum (NYSE:AMTM)

With operations spanning approximately 80 countries and a workforce of specialized engineers and technical experts, Amentum Holdings (NYSE:AMTM) provides advanced engineering and technology solutions to U.S. government agencies, allied governments, and commercial enterprises across defense, energy, and space sectors.

Amentum reported revenues of $3.42 billion, up 2.3% year on year. This result beat analysts’ expectations by 2.1%. Overall, it was a very strong quarter as it also put up a solid beat of analysts’ EPS estimates.

Amentum had the slowest revenue growth and weakest full-year guidance update among its peers. The stock is down 15.5% since reporting and currently trades at $17.33.

Read our full, actionable report on Amentum here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.