Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at Flex (NASDAQ:FLEX) and its peers.

The sector could see higher demand as the prevalence of advanced electronics increases in industries such as automotive, healthcare, aerospace, and computing. The high-performance components and contract manufacturing expertise required for autonomous vehicles and cloud computing datacenters, for instance, will benefit companies in the space. However, headwinds include geopolitical risks, particularly U.S.-China trade tensions that could disrupt component sourcing and production as the Trump administration takes an increasingly antagonizing stance on foreign relations. Additionally, stringent environmental regulations on e-waste and emissions could force the industry to pivot in potentially costly ways.

The 9 electronic components & manufacturing stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 5.1% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 2.2% on average since the latest earnings results.

Flex (NASDAQ:FLEX)

Originally known as Flextronics until its 2016 rebranding, Flex (NASDAQ:FLEX) is a global manufacturing partner that designs, engineers, and builds products for companies across industries from medical devices to solar trackers.

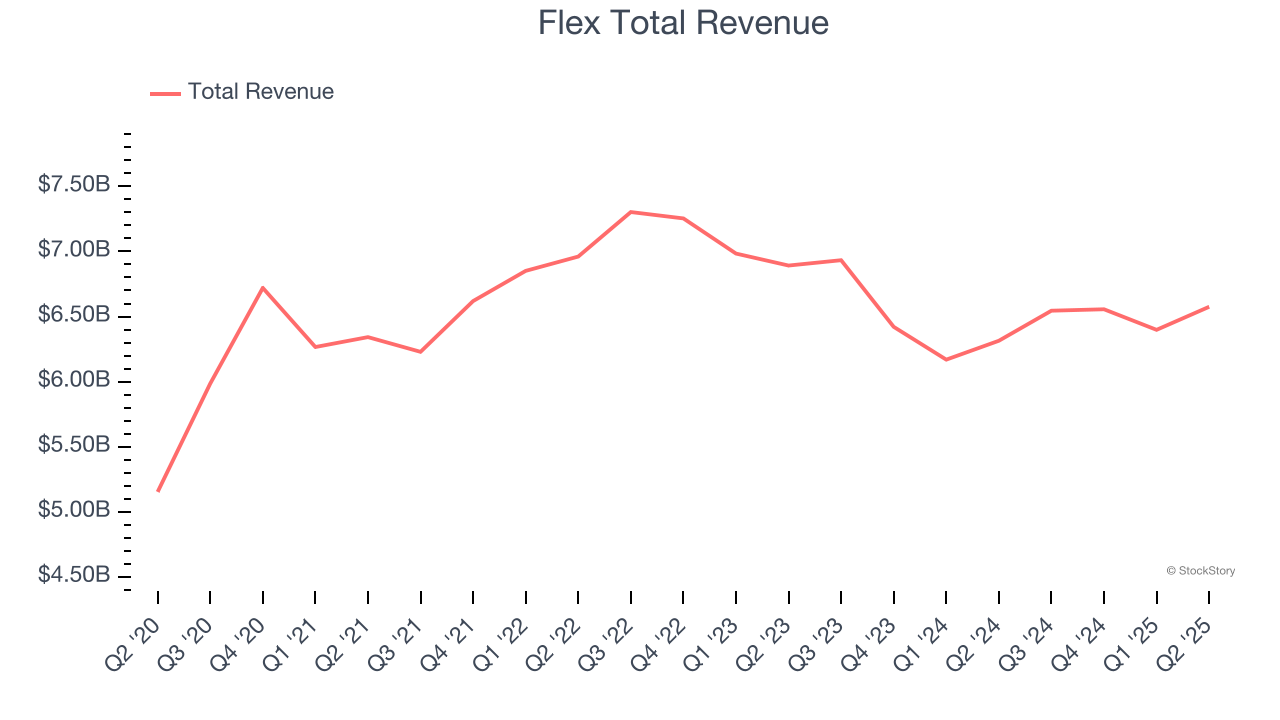

Flex reported revenues of $6.58 billion, up 4.1% year on year. This print exceeded analysts’ expectations by 4.9%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ EPS estimates and a narrow beat of analysts’ EPS guidance for next quarter estimates.

"Our first quarter results are a great start to FY26 and a testament to the strength of our strategic focus on high-growth end-markets like data center and power," said Revathi Advaithi, CEO of Flex.

Unsurprisingly, the stock is down 6.4% since reporting and currently trades at $50.35.

Is now the time to buy Flex? Access our full analysis of the earnings results here, it’s free.

Best Q2: TTM Technologies (NASDAQ:TTMI)

As one of the world's largest printed circuit board manufacturers with facilities spanning North America and Asia, TTM Technologies (NASDAQ:TTMI) manufactures printed circuit boards (PCBs) and radio frequency (RF) components for aerospace, defense, automotive, and telecommunications industries.

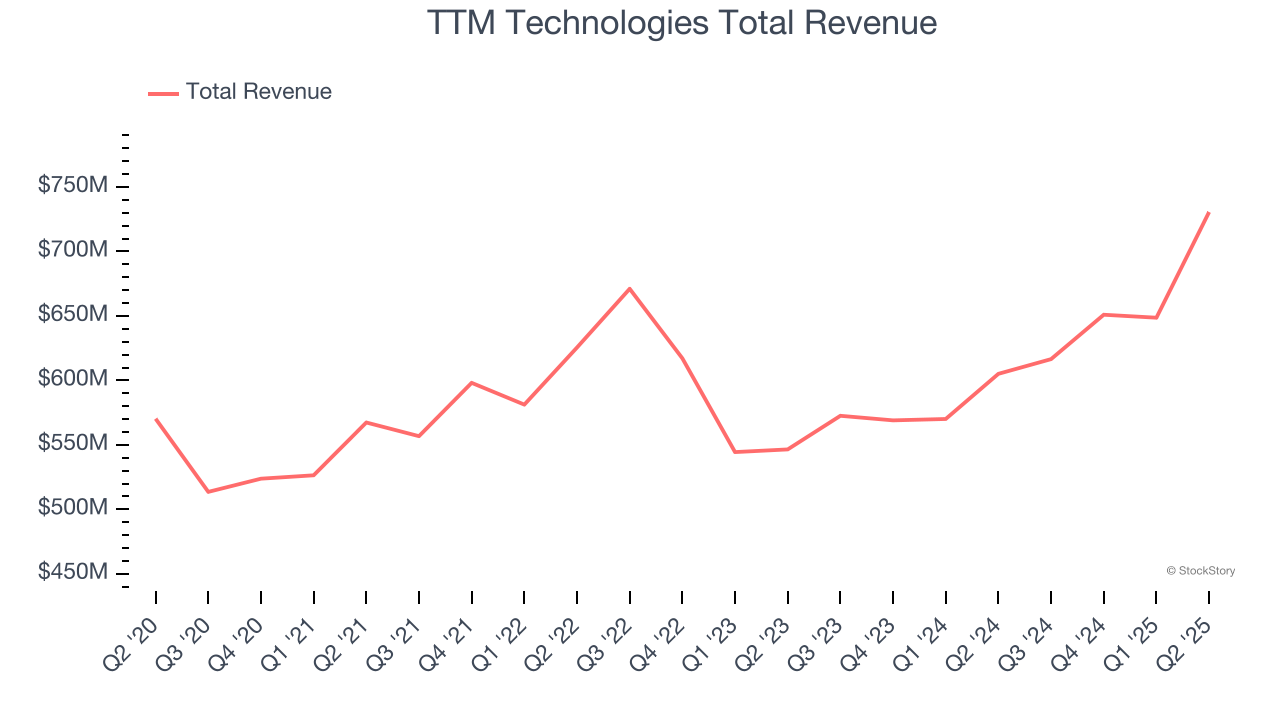

TTM Technologies reported revenues of $730.6 million, up 20.7% year on year, outperforming analysts’ expectations by 9%. The business had an exceptional quarter with a solid beat of analysts’ EPS guidance for next quarter estimates and an impressive beat of analysts’ EPS estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 8.1% since reporting. It currently trades at $44.80.

Is now the time to buy TTM Technologies? Access our full analysis of the earnings results here, it’s free.

Slowest Q2: Rogers (NYSE:ROG)

With roots dating back to 1832, making it one of America's oldest continuously operating companies, Rogers (NYSE:ROG) designs and manufactures specialized engineered materials and components used in electric vehicles, telecommunications, renewable energy, and other high-performance applications.

Rogers reported revenues of $202.8 million, down 5.3% year on year, exceeding analysts’ expectations by 2%. Still, it was a slower quarter as it posted a significant miss of analysts’ EPS guidance for next quarter estimates and a significant miss of analysts’ EPS estimates.

Interestingly, the stock is up 6.5% since the results and currently trades at $69.85.

Read our full analysis of Rogers’s results here.

Knowles (NYSE:KN)

With roots dating back to 1946 and a focus on components that must perform flawlessly in critical situations, Knowles (NYSE:KN) designs and manufactures specialized electronic components like high-performance capacitors, microphones, and speakers for medical technology, defense, and industrial applications.

Knowles reported revenues of $145.9 million, down 28.7% year on year. This result topped analysts’ expectations by 4.4%. Overall, it was a very strong quarter as it also put up a solid beat of analysts’ EPS guidance for next quarter estimates and revenue guidance for next quarter slightly topping analysts’ expectations.

Knowles had the slowest revenue growth among its peers. The stock is up 5.6% since reporting and currently trades at $19.70.

Read our full, actionable report on Knowles here, it’s free.

Plexus (NASDAQ:PLXS)

With over 20,000 team members across 26 global facilities, Plexus (NASDAQ:PLXS) designs, manufactures, and services complex electronic products for companies in aerospace/defense, healthcare, and industrial sectors.

Plexus reported revenues of $1.02 billion, up 6% year on year. This print was in line with analysts’ expectations. It was a strong quarter as it also recorded an impressive beat of analysts’ EPS estimates and a decent beat of analysts’ EPS guidance for next quarter estimates.

Plexus had the weakest performance against analyst estimates among its peers. The stock is down 4% since reporting and currently trades at $128.51.

Read our full, actionable report on Plexus here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.