The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how modern fast food stocks fared in Q2, starting with Sweetgreen (NYSE:SG).

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

The 7 modern fast food stocks we track reported a slower Q2. As a group, revenues missed analysts’ consensus estimates by 1.2%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 12.6% since the latest earnings results.

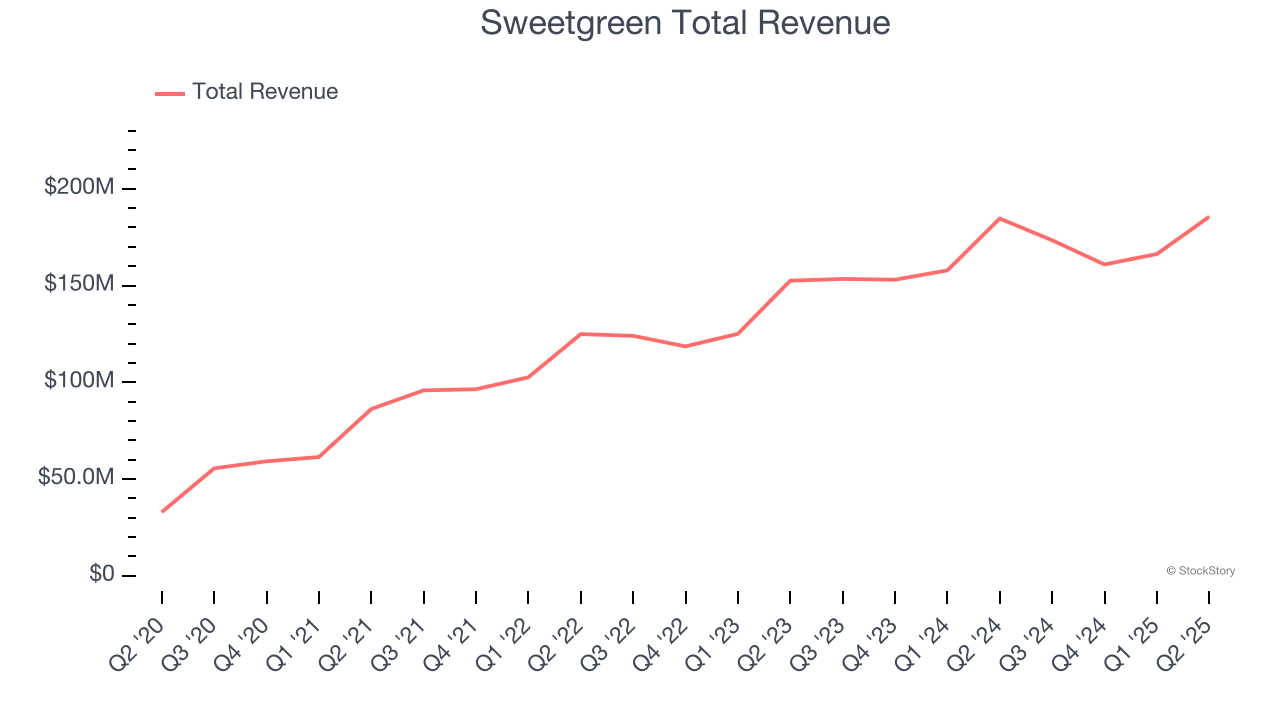

Sweetgreen (NYSE:SG)

Founded in 2007 by three Georgetown University alum, Sweetgreen (NYSE:SG) is a casual quick service chain known for its healthy salads and bowls.

Sweetgreen reported revenues of $185.6 million, flat year on year. This print fell short of analysts’ expectations by 3.3%. Overall, it was a disappointing quarter for the company with full-year revenue guidance missing analysts’ expectations.

Sweetgreen delivered the weakest full-year guidance update of the whole group. Unsurprisingly, the stock is down 26% since reporting and currently trades at $9.36.

Read our full report on Sweetgreen here, it’s free.

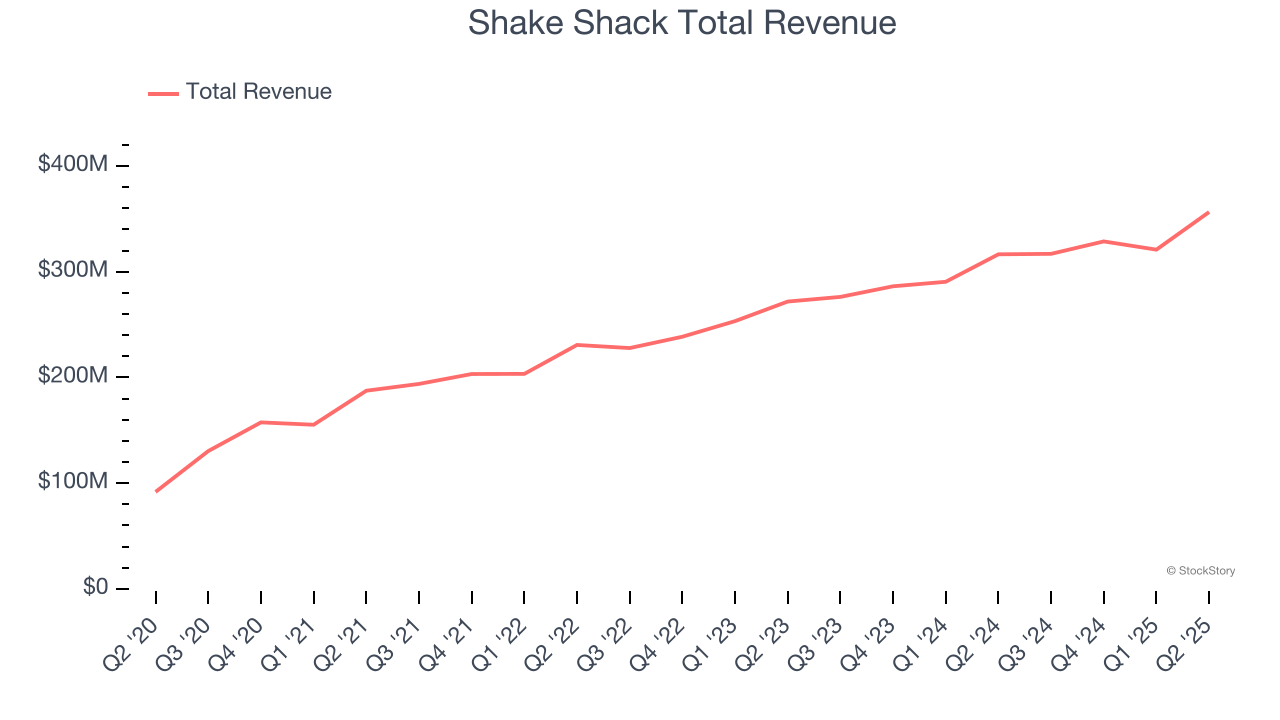

Best Q2: Shake Shack (NYSE:SHAK)

Started as a hot dog cart in New York City's Madison Square Park, Shake Shack (NYSE:SHAK) is a fast-food restaurant known for its burgers and milkshakes.

Shake Shack reported revenues of $356.5 million, up 12.6% year on year, outperforming analysts’ expectations by 0.9%. The business had a strong quarter with an impressive beat of analysts’ EBITDA estimates and a beat of analysts’ EPS estimates.

Shake Shack delivered the biggest analyst estimates beat among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 25.5% since reporting. It currently trades at $105.04.

Is now the time to buy Shake Shack? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Noodles (NASDAQ:NDLS)

Offering pasta, mac and cheese, pad thai, and more, Noodles & Company (NASDAQ:NDLS) is a casual restaurant chain that serves all manner of noodles from around the world.

Noodles reported revenues of $126.4 million, flat year on year, falling short of analysts’ expectations by 3.9%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and a significant miss of analysts’ EBITDA estimates.

Noodles delivered the highest full-year guidance raise but had the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 26.1% since the results and currently trades at $0.75.

Read our full analysis of Noodles’s results here.

CAVA (NYSE:CAVA)

Starting from a single Washington, D.C. location, CAVA (NYSE:CAVA) operates a fast-casual restaurant chain offering customizable Mediterranean-inspired dishes.

CAVA reported revenues of $280.6 million, up 20.2% year on year. This result missed analysts’ expectations by 1.8%. Overall, it was a slower quarter as it also recorded a significant miss of analysts’ same-store sales estimates and full-year EBITDA guidance missing analysts’ expectations.

CAVA delivered the fastest revenue growth among its peers. The stock is down 17.6% since reporting and currently trades at $69.75.

Read our full, actionable report on CAVA here, it’s free.

Potbelly (NASDAQ:PBPB)

With a unique origin story where the company actually started as an antique shop, Potbelly (NASDAQ:PBPB) today is a chain known for its toasty sandwiches.

Potbelly reported revenues of $123.7 million, up 3.4% year on year. This number surpassed analysts’ expectations by 0.9%. Overall, it was a strong quarter as it also logged a solid beat of analysts’ EBITDA estimates and full-year EBITDA guidance topping analysts’ expectations.

The stock is up 7.6% since reporting and currently trades at $12.41.

Read our full, actionable report on Potbelly here, it’s free.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.